The era of "subsidized AI" may be coming to an end

What changed. For most of 2024 and 2025, “AI agents are expensive” was a thesis. There were anecdotes: a leaked memo here, an enthusiast forum post there. The numbers were not concrete enough to publish in a Big Four CFO guide or anchor a podcast episode. That changed in Q1 and Q2 of 2026. Real enterprises published real numbers. Two of the largest coding-agent surfaces shifted their billing model in the same quarter. Deloitte put “token economics” on the CFO finance agenda. The cost discipline layer of the agent operations stack (what the 9-layer ecosystem map called layer 9) was a category looking for an owner six weeks ago. It is now a category with several published seven- and eight-figure cost shocks and a hard timeline for when individual developers will start feeling token consumption directly.

This post collects the data.

The numbers that are no longer hypothetical

Microsoft. In December 2025, Microsoft rolled Claude Code out to engineers, product managers, and designers across the company. By spring, the tool had spread well beyond engineering. In late May 2026, Microsoft began quietly cancelling those Claude Code licenses inside its Experiences and Devices group, the division that builds Windows, Microsoft 365, Outlook, Teams, and Surface. Affected engineers must migrate to GitHub Copilot CLI by June 30, the last day of Microsoft’s fiscal year. The Verge had the original scoop; Windows Central, Fortune, and The Next Web followed. The official reason is toolchain unification. The timing is at fiscal-year-end. Microsoft, of any company, is best positioned to know what enterprise-scale Claude Code usage actually costs; its engineers were among the heaviest users outside Anthropic’s direct customer base. If the unit economics had improved with scale, this would have been the quarter Microsoft locked in a multi-year deal at favourable terms. Instead, it is unwinding the experiment on a deadline that closes the books on FY26. When the company with the most leverage in the room walks away from a vendor whose product its own staff prefer, the signal is not about preference.

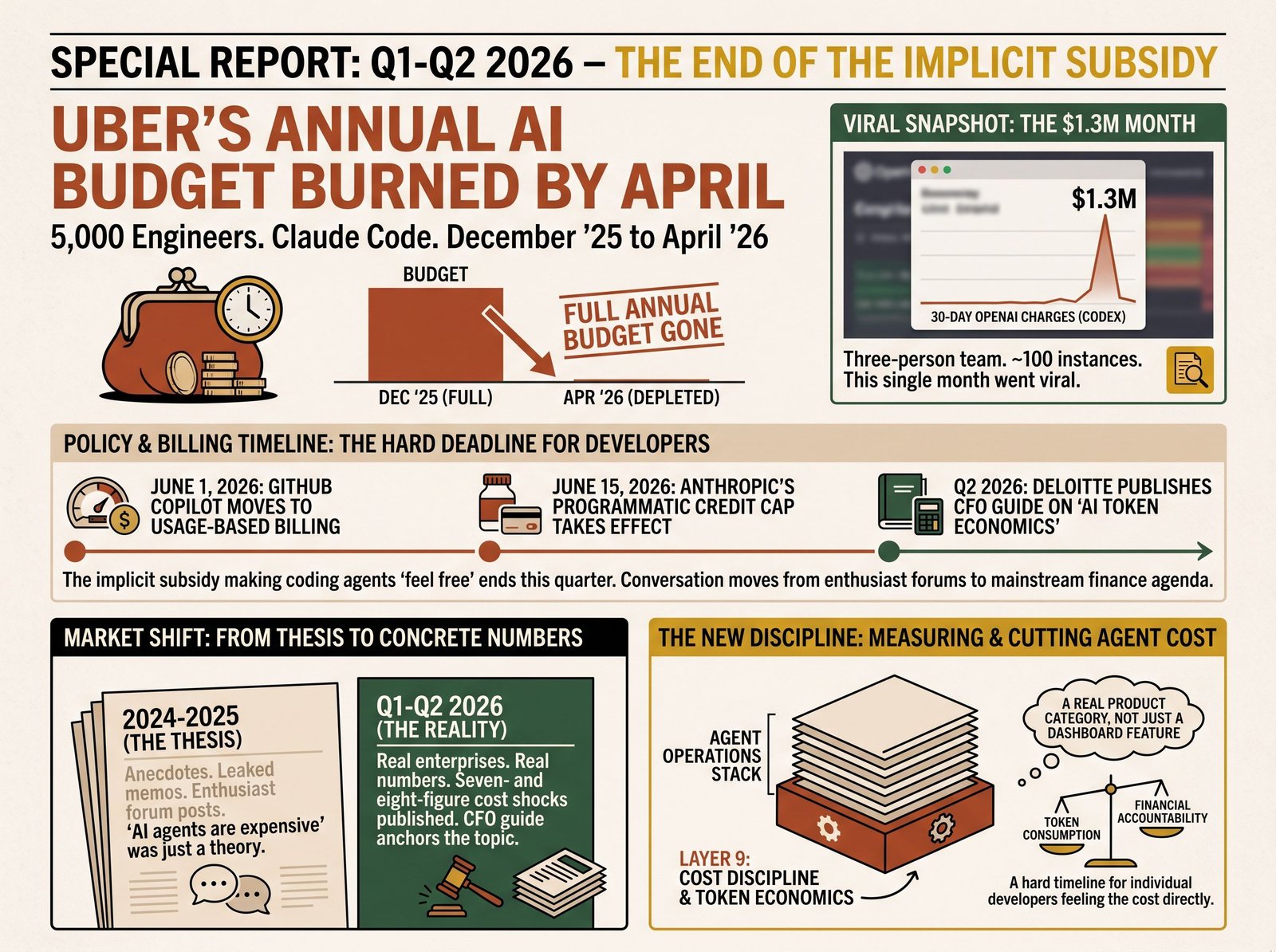

Uber. In December 2025, Uber gave roughly 5,000 engineers access to Claude Code. By April 2026, four months later, the company had burned through its entire annual AI budget. Not half, not three-quarters; the full year’s allocation, gone before the second quarter ended. Adoption hit 84% of engineers by March and 95% by spring; individual costs ran $500-$2,000 per engineer per month, well above projections. This is Uber’s CTO talking about it publicly, not a leaked memo. Vantage’s analysis and Deloitte’s April 2026 CFO guide both reference the same numbers.

OpenClaw / Peter Steinberger (May 2026). Steinberger posted a screenshot showing $1,305,088.81 in OpenAI API charges over 30 days: 603 billion tokens, 7.6 million requests, across roughly 100 Codex instances run by a three-person team. Steinberger joined OpenAI in February, and OpenAI is covering the bill, but the screenshot circulated widely as the cleanest single data point on what unattended coding-agent infrastructure can cost when run near saturation. He later clarified that the $1.3M figure reflects Codex “Fast Mode” pricing, which consumes credits much faster than standard execution; the same workload at standard rates would have come to roughly $300K. Tom’s Hardware, The Next Web, and a long tail of outlets picked it up. This is the most-cited cost figure in the category right now, and it broke this month.

An anonymized healthcare enterprise. Consumed one trillion tokens over six months, translating into more than $6 million in unplanned costs before the finance team had a clear picture of what was driving the spend. The story was published by elvex.com as an anonymized case study, with enough detail for the figures to be verifiable.

The leanopstech audit. Between March and May 2026, leanopstech audited 30 engineering teams running agentic AI in production. Three findings stand out. There was a 20× cost spread between p10 and p90 developers using the same tool: same agent, same access, an order of magnitude apart in consumption. Re-sent context accounted for 62% of the average team’s bill: most of the token spend was not doing useful work, it was retransmitting the same project context call after call after call. And a single developer on one of the audited teams ran up $4,200 in API fees over a long weekend during one autonomous refactoring session. The average agentic developer using Claude Code or Cursor was spending $400-$1,500/month, with extreme cases hitting $4,000+ in days.

These five stories are not isolated. They are the visible tip of a conversation now happening inside every engineering organization above 200 people. The pattern across them is consistent. Agents are doing more work without supervision. Costs scale with autonomy. The existing tooling for tracking spend lags behind the spend itself, which means the discovery of a cost problem happens after the cost has already accrued, not before.

The structural pivot happening this quarter

Two billing changes hit in the same 15-day window.

GitHub Copilot moves to usage-based billing on June 1, 2026. Copilot Business stays at $19/seat with $19 of monthly AI Credits included; Copilot Enterprise stays at $39/seat with $39 of credits. The change is in the metering: every plan now consumes credits per token (input, output, and cached tokens, at rates that vary by model), with code-completion and Next Edit suggestions still included for free. Credits are pooled across the organization rather than stranded per user, agentic features and Cloud Agent runs draw from the same pool, and admins can set budgets at the enterprise, cost-center, and user levels. Power users who were previously burning 10× the team average without anyone noticing will now show up on a dashboard somewhere.

Anthropic introduces a programmatic credit cap on subscription plans on June 15, 2026. Pro plans get $20 of API-equivalent credits per cycle, Max 5x gets $100, Max 20x gets $200. Past the cap, full API rates apply. The cap covers programmatic Claude use (Claude Agent SDK, claude -p, Claude Code GitHub Actions, and third-party apps built on the SDK) while interactive use (Claude.ai chat, Claude Code used interactively in the terminal) stays on the existing subscription limits. For a developer who was running Claude Code unattended on a flat-rate Max 20x subscription, the second half of every cycle now meters against per-token billing.

Two of the largest coding-agent surfaces on the market are ending the implicit subsidy in the same quarter. This was not coordinated, but the effect is. June 15 is approximately when “AI agents feel free” stops being broadly true.

Why this just became mainstream

The signal that a topic has crossed from enthusiast to mainstream is when accounting firms publish frameworks for it. Deloitte published a CFO guide on AI token economics in April 2026. Twelve months ago, “token cost” was not a finance-function topic. Today there is a Big Four publication framework for it, alongside a companion piece on how CTOs can manage tokenomics. The Pragmatic Engineer covered the same story in May. Reddit threads about token bills routinely hit four-digit upvote counts on r/LocalLLaMA and r/MachineLearning. The discourse is no longer specialized; the buyer for cost optimization has moved from “interested individual” to “engineering leader with a real budget problem.”

There is also a regulatory dimension worth flagging. Articles 9, 15, and 72 of the EU AI Act (continuous risk management, demonstrable accuracy and robustness, and post-market monitoring respectively) are now being read against the operational characteristics of agent deployments inside EU enterprises. “AI governance token cost” has become a regulatory line item, not just a finance one, for a meaningful subset of the European market.

What this means

A few things follow from this shift.

The category of cost discipline for agents (measuring it, attributing it, predicting it, reducing it) has become a real product space. It is not a checkbox feature inside an observability dashboard. The buyer is real: engineering leadership, FinOps, platform teams, AI program owners. The pain is now public: Microsoft, Uber, OpenClaw, the healthcare enterprise. The timeline is hard: June 1 and June 15 for usage-billing changes, June 30 for the Microsoft migration deadline. The regulatory pressure is real: Articles 9, 15, 72.

The companies that solve this problem own a layer of the agent operations stack that did not have an obvious owner six months ago. The 9-layer map called this out as the most underbuilt of the nine layers. The news of the past quarter just locked the timeline. Cost dashboards report what happened. Cost-optimization recommendations validated against a team’s own data tell that team what to change. The gap between those two things is most of the actual value to be captured.

The shift from “interesting research category” to “live, urgent, regulated category” happened faster than most people in this space expected. June will be the month it becomes visible to every Copilot and Claude Code user, not just the ones who already paid attention.

Common questions

- Why is the Microsoft retreat such a big signal?

- Two reasons. First, scale: Microsoft's Experiences and Devices org runs Windows, M365, Outlook, Teams, and Surface. Their engineers were among the heaviest Claude Code users on the planet outside Anthropic's direct customer base, which means Microsoft had better data on enterprise-scale Claude Code economics than almost anyone. Second, incentives: GitHub (Microsoft-owned) is the direct competitor to Claude Code through Copilot CLI. If the unit economics had improved with usage, this would have been the quarter Microsoft locked in a multi-year deal at favorable terms. They had the leverage. Instead they unwound the experiment on a deadline that closes the books on fiscal year. The Verge had the original scoop; Windows Central, Fortune, and The Next Web followed. The official line is toolchain unification; the unofficial reason is in the calendar.

- Are these numbers verifiable?

- Mostly yes, with one caveat. The Uber, leanopstech, and Deloitte figures are from named public sources (Fortune, elvex.com case studies, the Deloitte CFO guide). The OpenClaw screenshot is verifiable in that the screenshot exists and circulated widely; Steinberger published it himself and several outlets covered it (note the Fast Mode caveat above). The healthcare-enterprise figure is anonymized in elvex's case study, so it cannot be checked against an identifiable account, but their reporting in this category is well-sourced. Any specific number is a snapshot of one team's setup, and the same team running the same agents next quarter would produce different figures.

- Is this just a coding-agent problem, or does it hit other agent types too?

- Coding agents are loudest because they are easiest to measure and the early adopters skew toward visibility (engineers post their bills). The pattern hits any long-running, tool-using agent: research agents, customer-support agents in pilot, browser-automation agents, autonomous data-pipeline agents. The economic shape is the same: costs scale with autonomy, and most teams discover the cost problem only after it has accrued.

- Why didn't the existing observability tools catch this?

- They caught the symptoms; they could not surface the underlying behavior. Cost dashboards in Langfuse, LangSmith, Helicone, and the provider consoles all show spend over time. None of them tell you that 62% of your bill is re-sent context, or that a particular session pattern would have completed acceptably on a cheaper model. That gap between 'here is the bill' and 'here is what to change about the bill' is the actual layer-9 work.

- What about Anthropic users on the Pro plan?

- Pro plans get a $20 programmatic credit pool per cycle, after which full API rates apply. For a light user, $20 covers a normal month easily. For a developer running Claude Code several hours a day, $20 is a few days of headroom. The credit cap mostly affects power users on Pro and the entire Max 5x / Max 20x tier; light users on Pro probably will not notice the change.

- Is this a temporary squeeze, or is the trajectory permanent?

- Short-term, both Anthropic and the model providers in general could walk back policies: credit caps could expand, subscription rates could absorb more value, Copilot UBB could absorb more under the seat price. Longer-term, the trajectory is not reversible. Agents are getting more autonomous, sessions are running longer unattended, and provider margins on subsidized usage are not infinite. Whatever happens to the specific policies announced for June, the structural shift toward 'agent users feel their token consumption directly' is the multi-year direction.